Great (Rate) Expectations: Navigating the Path Forward

A rising tide that lifts all funded status

Over the past three months, US equities have hit historical highs, the US Treasury curve has steepened rapidly and there has been increased volatility in interest rates, driven mainly by inflation expectations. Since the beginning of 2021, expectations around the US economy reopening and increased growth have continued to improve with the accelerating pace of COVID-19 vaccinations and continued supportive monetary and fiscal policies. Meanwhile, as rates have creeped higher, the looming question is how much more can they run and, subsequently, is now the time to be buying more fixed income?

In Great Expectations, Charles Dickens’ character Mr. Jagger famously advises Pip to “take nothing on its looks; take everything on evidence.” To begin answering these questions, it may be helpful to heed Dickens’ advice to look beyond the assumptions and perceptions and to consider the facts. For plan sponsors today, it is imperative to look beyond this recent appearance of rising rates and assess the impact of their current interest rate risk exposure while evaluating the pros/cons of taking advantage of current market expectations.

The outlook for real growth continues to improve with the pace of the vaccinations and the trajectory of consumer spending and reopening. It seems inevitable that the Fed will need to shift more hawkish at some point in the future. At the same time, as significant fiscal stimulus and accommodative monetary policy have been the major themes of the last twelve months, concerns about inflation seem to dominate market sentiment.

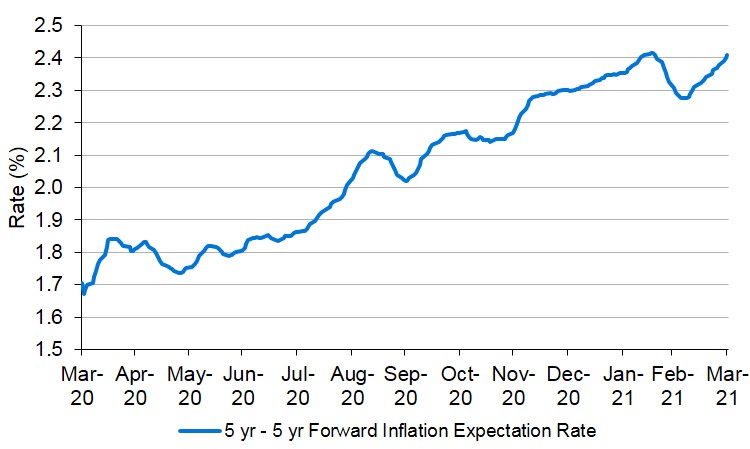

In fact, looking at the 5-year-5-year forward inflation rate in Figure 1, we can see there has been an increased amount of volatility in inflation expectations since the beginning of 2021 (i.e. a large dip in February followed a surge in March). What this volatility in inflation expectations may suggest is that the market is laser-focused on upside inflation risks in the near term and this overstatement may have contributed to the surge in rates since the beginning of the year.

Figure 1: 5Y – 5Y Forward inflation expectation rate

Source: LGIM America, Citi.

If inflation expectations have indeed run too far, too fast, we should question the sustainability of increasing rates. With central banks reaffirming their commitment to keeping policy rates anchored near zero, the upward pressure on inflation may prove to be relatively limited, especially in an economy that is not yet operating at full capacity. An expected increase in inflation, due to rising real growth, is broadly healthy for risk assets while, in contrast, an economy being lifted by excess debt creation and other loose monetary policy actions could be negative for certain asset classes. As plan sponsors weigh the decision of whether to reduce equity and increase allocations to fixed income, these factors are important to consider.

To hedge more or to not to hedge more

As funding positions of plans have seen dramatic improvements in 2021, many plans have hit rebalancing and derisking triggers. Some have stuck to their previously charted asset allocation plans and hedging glidepaths. Others have stepped back and asked, “Should we really buy today if rates are going to continue to rise?”

In our opinion, there are two key questions for each investor to ask themselves. One, how valuable are the benefits of further increases in rates? And two, how convicted are you that interest rates will continue to rise? On the former, we have seen a few clients reach that nirvana spot of being fully funded on a plan termination basis where that is their ultimate goal. In this scenario, there is not any more upside left and it is best to take the chips off the table.

For other clients, the rise in rates has been accompanied by an improvement in their funding position, but the long-term economics would continue to improve further from additional increases in rates. On the second question, we remain humbled by the claim that predicting the direction of interest rates is not a well-compensated proposition. While there are reasons to believe we are headed to higher rates over the longer term, there are other scenarios that could result in a revisiting of the lows of last year.

Without strong conviction on the pathway, we generally advocate for hedging interest rate risk. We have many clients that have adopted this belief and are content for having done so as it's allowed them to focus on their core businesses. With this said, we can understand that the timing of when to cover this risk is an important decision for those that have not fully done so to date.

For plan sponsors looking to decrease funded status volatility, hedging interest rate risk is generally accepted as a sensible path. If one believes that rates will continue to rise and elevated inflation expectations are both realistic and sustainable, buying fixed income now may prove painful in the short term. On the other hand, a view that inflation expectations are ahead of themselves may be reason to believe there could be sustained volatility in rates, in turn providing opportunities for active fixed income managers to find attractive entry points and alpha generation. Further, with equity valuations near all-time highs, actively managed fixed income in an increasing rate environment can add additional income and diversification to an asset allocation.

Let the game come to you

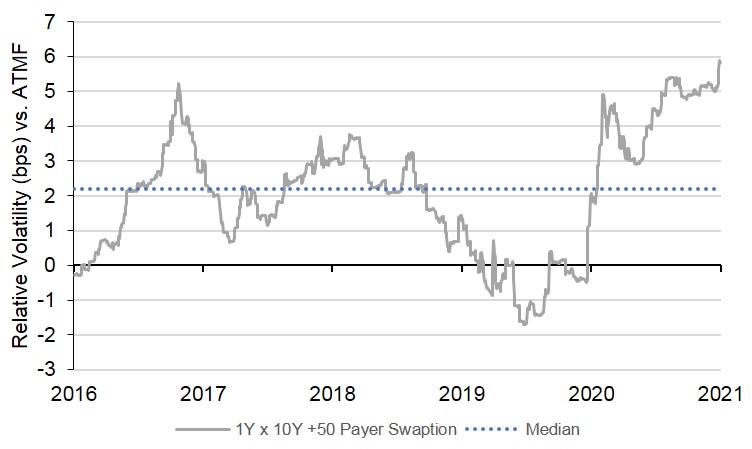

For plans that are not fully hedged, but whose strategic path is to increase hedging over time, swaptions provide a way to commit now to buying more duration in the future. With all that has transpired, the market is pricing in a statistically significant amount of interest rate volatility, making the levels at which a plan can enter these positions attractive. Figure 2 depicts that the implied volatility of an illustrative swaption is two standard deviations above its five-year median. The following examples use swaptions as an implementation tool, but similar increased volatility dynamics exist in other interest rate option markets as well (e.g. options on TLT, the iShares 20+ Treasury ETF).

Figure 2: 1Y x 10Y Payer swaption volatility

Source: LGIM America, Barclays.

One method for a pension plan to monetize a future glidepath step now is by selling out-of-the-money payer swaptions; selling the counterparty the right, but not the obligation, to pay the plan fixed rates if the referenced tenor rate goes above a certain level. In other words, upon exercise, the plan receives fixed rate payments, economically akin to owning a similar maturity fixed rate bond. Swaptions can also be cash settled at expiry, allowing the plan to use the proceeds to purchase a physical Treasury if preferable to an interest rate swap position. Not only can this be a set way to implement a hedging glidepath as interest rates rise, the plan also is paid a premium to do so, at a statistically significant level.

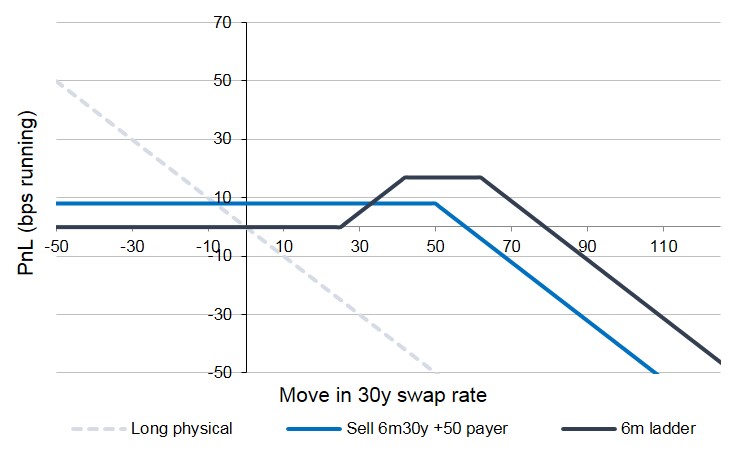

The solid blue line in Figure 3 depicts the payoff profile of selling a payer swaption struck at 50 basis points above current spot rates and illustrates that if rates increase by more than 50 basis points at expiration, the outcome is economically equivalent to buying a physical fixed rate bond.

Some investors hold a view that rates will move somewhat higher, but inflation will be relatively contained and the Fed will thread the hiking needle successfully. A payer ladder can be an efficient, costless expression of this view. This can be implemented with a combination of buying and selling payer swaptions at certain levels above the forward rate. The solid black line in Figure 3 shows how an investor can profit if over six months the 30-year swap rate rises approximately 26 basis points, with gains maximized if the 30-year swap rate ends up between approximately 40 and 60 basis points higher. If the 30-year swap rate increases by more than approximately 60 basis points, the plan would enter their hedge and the payoff profile becomes economically akin to owning a fixed rate bond.

Figure 3: Swaption payoff profiles

Source: LGIM America, Bloomberg.

At LGIM America, our goal is to help our clients identify and quantify different approaches to assist in developing and executing solutions that meet their plan’s needs and views. If you have questions or considerations you are exploring in this market environment, please reach out to our team.

Disclosures

This material is intended to provide only general educational information and market commentary. Views and opinions expressed herein are as of April 2021 and may change based on market and other conditions. The material contained here is confidential and intended for the person to whom it has been delivered and may not be reproduced or distributed. The material is for informational purposes only and is not intended as a solicitation to buy or sell any securities or other financial instrument or to provide any investment advice or service. Legal & General Investment Management America, Inc. does not guarantee the timeliness, sequence, accuracy or completeness of information included. Past performance should not be taken as an indication or guarantee of future performance and no representation, express or implied, is made regarding future performance.

We have more blogs to share

Visit our blog site to explore our latest views on markets, investment strategy and long-term themes.